Gerardo Del Real,

Editor

Jan. 20, 2026

Gold is doing what gold always does in moments like this.

It’s protecting capital. It’s signaling geopolitical turbulence.

And it’s reminding investors that hard assets matter when governments overspend, currencies weaken, and confidence erodes.

But if you’re looking for the next gold — the asset with the kind of imbalance that doesn’t just preserve wealth but creates outsized upside — you should be paying very close attention to uranium.

Because while gold’s bull market is widely understood, uranium’s is still being underestimated… even as the math underneath it has become impossible to ignore.

This Uranium Bull Market Is Built on Arithmetic

Strip away the noise and the narratives, and uranium comes down to a simple equation.

The global nuclear industry consumes roughly 185–200 million pounds of uranium per year.

For more than a decade, utilities have replaced less than half of what they burn annually through long-term contracts. The remainder has been pulled from inventories — inventories that are now widely acknowledged to be near multi-decade lows.

Since 2013, the global replacement rate has averaged roughly 45%.

In plain English: every year, utilities consume a pound of uranium and replace only about half a pound. The difference comes from stockpiles that are no longer abundant.

That imbalance has been building quietly for years. Now it’s visible.

The World Nuclear Association (WNA) — not known for alarmist forecasts — now projects a structural uranium deficit of roughly 70 million pounds per year through 2040, amounting to ~1.1 billion pounds of cumulative shortfall.

And this forecast stands before factoring in AI data centers, SMRs, or speculative demand scenarios.

This is the base case.

Demand Has Reset Higher — Permanently

One of the most important signals in this market is how dramatically long-term demand expectations have changed.

WNA’s current demand forecast for 2040 is 50% higher than what it projected just five years ago.

That kind of revision matters because uranium supply is slow, capital-intensive, and constrained by permitting, geopolitics, and long development timelines.

New mines don’t appear on command. They can take decades to prove up, get permits, and build.

When demand steps up this much, supply cannot respond quickly enough to prevent higher prices.

Utilities Delayed. Prices Moved Anyway.

Utilities have spent years trying to outwait the uranium market.

They pulled back on contracting, unhappy with prices that climbed from the $30s to the mid-$80s. Contracting volumes fell sharply even as prices continued to rise.

Recent history tells the story:

- 2022: ~115 million pounds contracted

- 2023: ~160 million pounds

- 2024: ~106 million pounds

- 2025 (through ~11 months): ~50–55 million pounds

That’s a fraction of annual demand.

The strategy was clear: delay purchases, pressure prices, wait for supply to appear.

Instead, prices climbed further.

Recent term contracts are being signed with fixed components near $88–$90, while market-linked structures carry ceilings well into the $130–$140 range. Those are the prices required to secure future pounds.

Utilities may not like it. But they’re running out of alternatives.

Supply Is Not Riding to the Rescue

Higher prices normally invite new supply. In uranium, that response has been muted.

Brownfield restarts have consistently underdelivered. ISR projects face rapid depletion and rising costs. Greenfield developments are scarce, slow, and politically complex.

Even optimistic supply scenarios still leave the market tens of millions of pounds short each year.

To meet projected demand by 2040, global production would need to rise to 390–530 million pounds annually.

There is no credible path to reach those levels using existing mines.

The Market Is Coiling Again

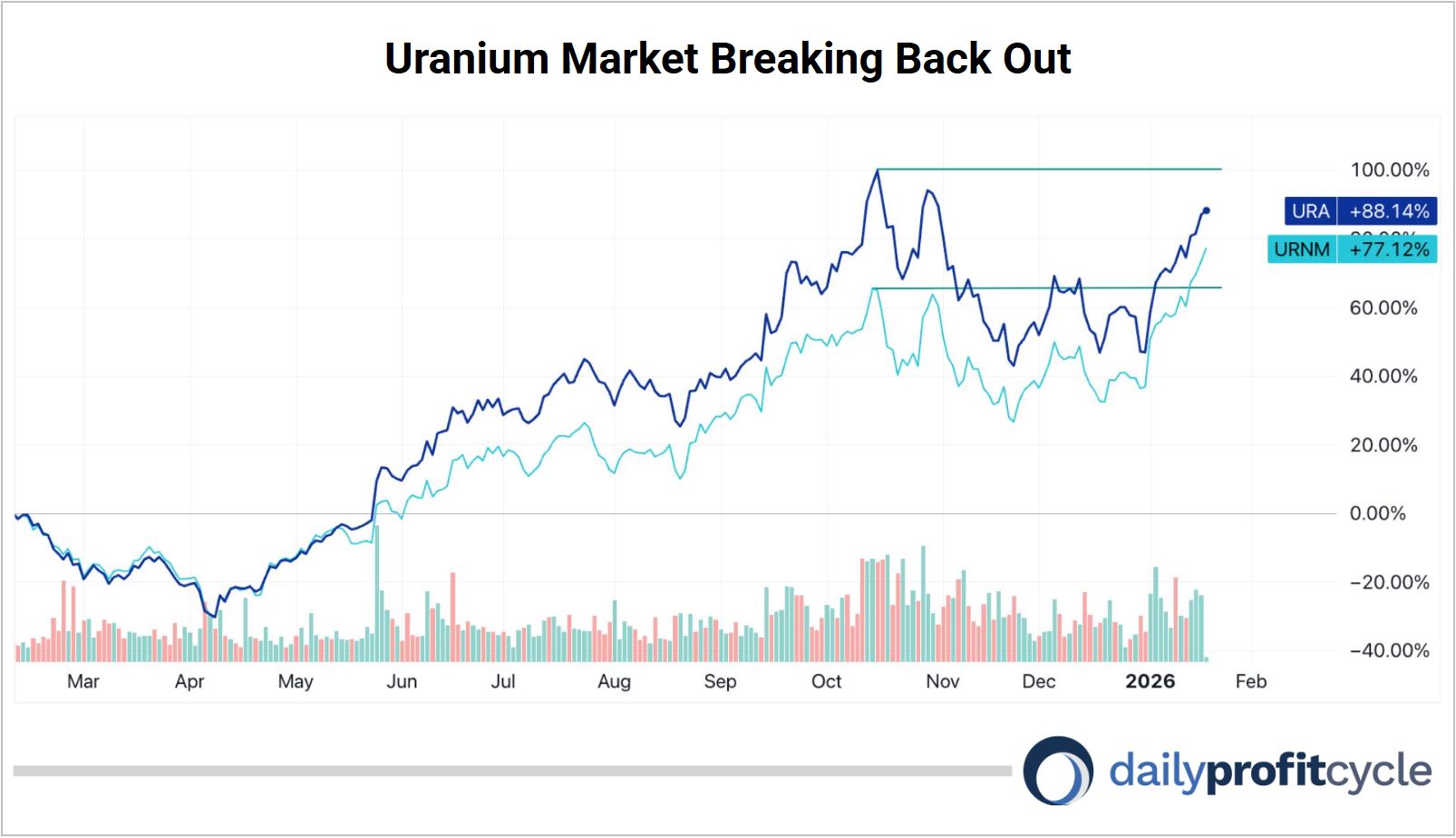

The equities are already signaling what’s coming next.

Over the past year, uranium stocks are up 60% to nearly 100% across the sector. Broad ETFs like URA and URNM confirm the strength of the move.

Yet over the last three months, prices have gone sideways.

That pause matters.

The chart shows uranium stocks consolidating just below their October highs — a classic setup after a strong advance. Volume has tightened. Volatility has compressed. Weak hands have exited.

This is how the next leg higher forms.

URNM is breaking back out because it holds physical pounds. Uranium stocks, particularly those that will provide the next round of supply, are next.

Why Uranium Deserves the Gold Comparison

Gold protects you from monetary disorder.

Uranium benefits from an energy system that has no viable substitute for reliable, baseload nuclear power.

Governments now classify uranium as a critical mineral. Supply chains are being reshored. Utilities can’t defer procurement indefinitely. Inventories are no longer a cushion. New supply takes years — often decades — to bring online.

Gold has history.

Uranium has a structural deficit backed by numbers.

And when markets like this finally resolve, they don’t drift higher. They reprice.

We’re no longer early.

But we’re positioned just ahead of the next breakout with these stocks.

As uranium stocks press against those October highs, the setup looks increasingly familiar.

The kind that precedes sustained, powerful moves.

And that’s why I believe uranium is setting up as the next great real-asset trade of this cycle.

See my full thesis and recommendations here.

Let's get it,

Gerardo Del Real

Editor, Daily Profit Cycle