Nick Hodge,

Publisher

Feb. 17, 2026

Editor’s Note: We’re seeing some chop and rotation in the markets. To help you figure out what’s going on, and to see what I’m buying amid ongoing stock market and commodity volatility, please check out the complimentary section from this month’s issue of Foundational Profits, below. The full issue contains every long-term position I own, how much of each position, and what I’m buying and selling this month. It’s available to members only.

Precious metals “crashed” over the past month — or so I heard.

Since the last issue, gold “tumbled” more than 10% and had its largest daily decline since the decade I was born (1980s).

And if gold plummeted, then silver “plummeted,” having put in its worst day (-27%) since the decade my parents were born (1960s).

Yet for all this crashing and tumbling and plummeting, gold remains up ~14% year-to-date. And silver’s up ~4%. That compares to an S&P that’s flat.

If those are crash-worthy numbers, then Bitcoin is dead in the gutter.

More important than the asset prices, our portfolio remains as insulated as a goose on a frozen pond.

The open portfolio is up more than 30% and, as I ran through the numbers this month, many positions are higher than they were when I compiled them last month.

Despite a volatility index that spiked above 20 in late January and early February, the S&P remains near all-time highs.

We remain bullish as we head toward the release of Q4 2025 gross domestic product on February 20th that will show continued growth in the economy. While we won’t see the +3.5% growth witnessed in Q2 and Q3 last year, it will be, on a quarter-over-quarter seasonally adjusted annual basis, closer to ~3%. Real GDP on a year-over-year basis should post its third consecutive quarter of expansion near 2.5% — up from 2.3% in Q3 —and expand again in the current quarter.

Inflation continues to cool as well, with January year-over-year CPI likely to come in near 2.5%, down from 2.68% in December. Expect similar levels for the balance of the year.

The economy is still expanding, but at a slower rate. And inflation is still abating, but also at a slower rate.

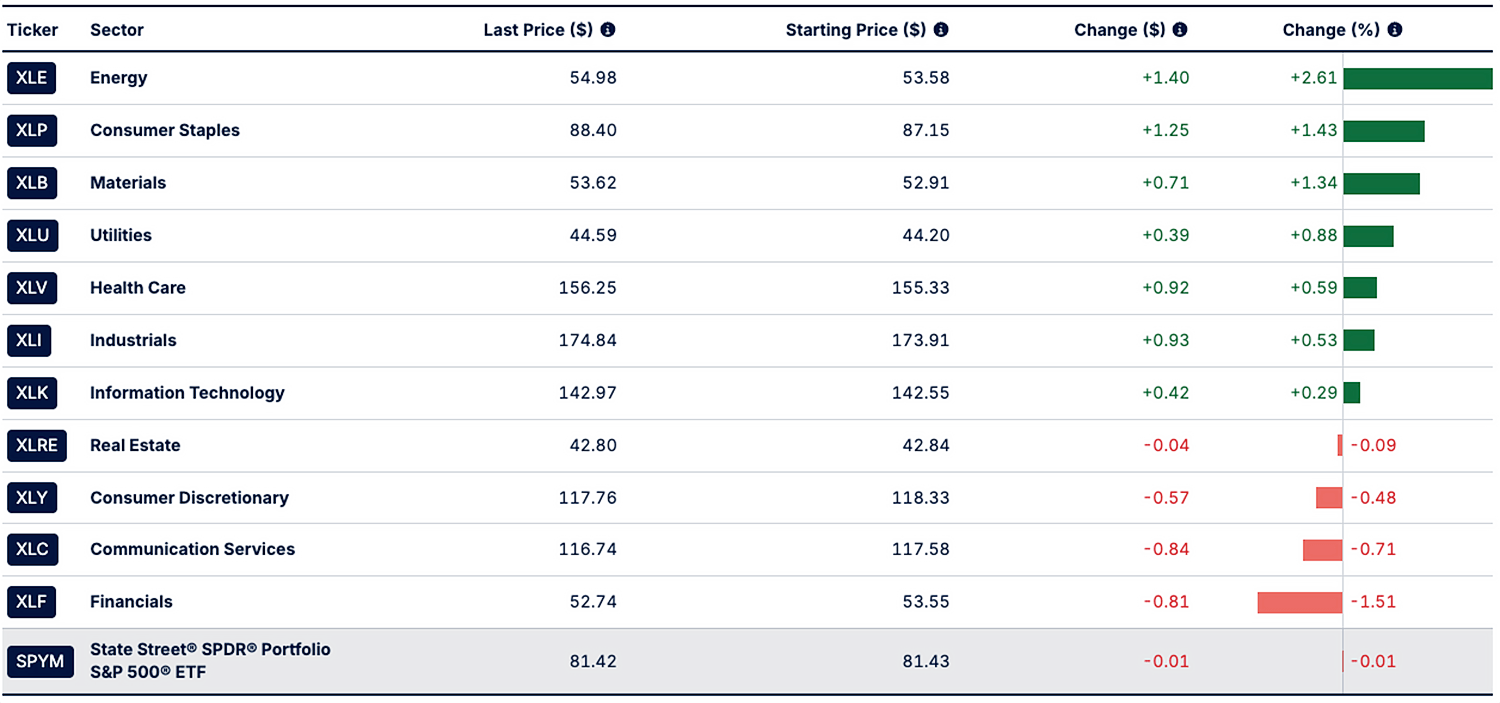

So while stock market bullishness remains, there is rotation afoot, with Information Technology and Communication Services negative for the year as of February 9th. We are now being led, thanks partially to a frigid East Coast winter and ongoing international geopolitical upheaval and uncertainty, by Energy and Materials, with a traditionally defensive Consumer Staple also in the top three.

On the interest rate front, the market temporarily misjudged incoming Fedhead Kevin Warsh as a hawk, which led to the aforementioned volatility as well as the “crash” in precious metals prices. More level chickenheads have since prevailed.

You won’t get a rate cut with Jerome still on the roost, with the market pricing in a ~92% chance of no cut in March and a 76% chance of no cut in April. But after he flies the coop in May, the market is showing a 48% chance of a quarter-point cut.

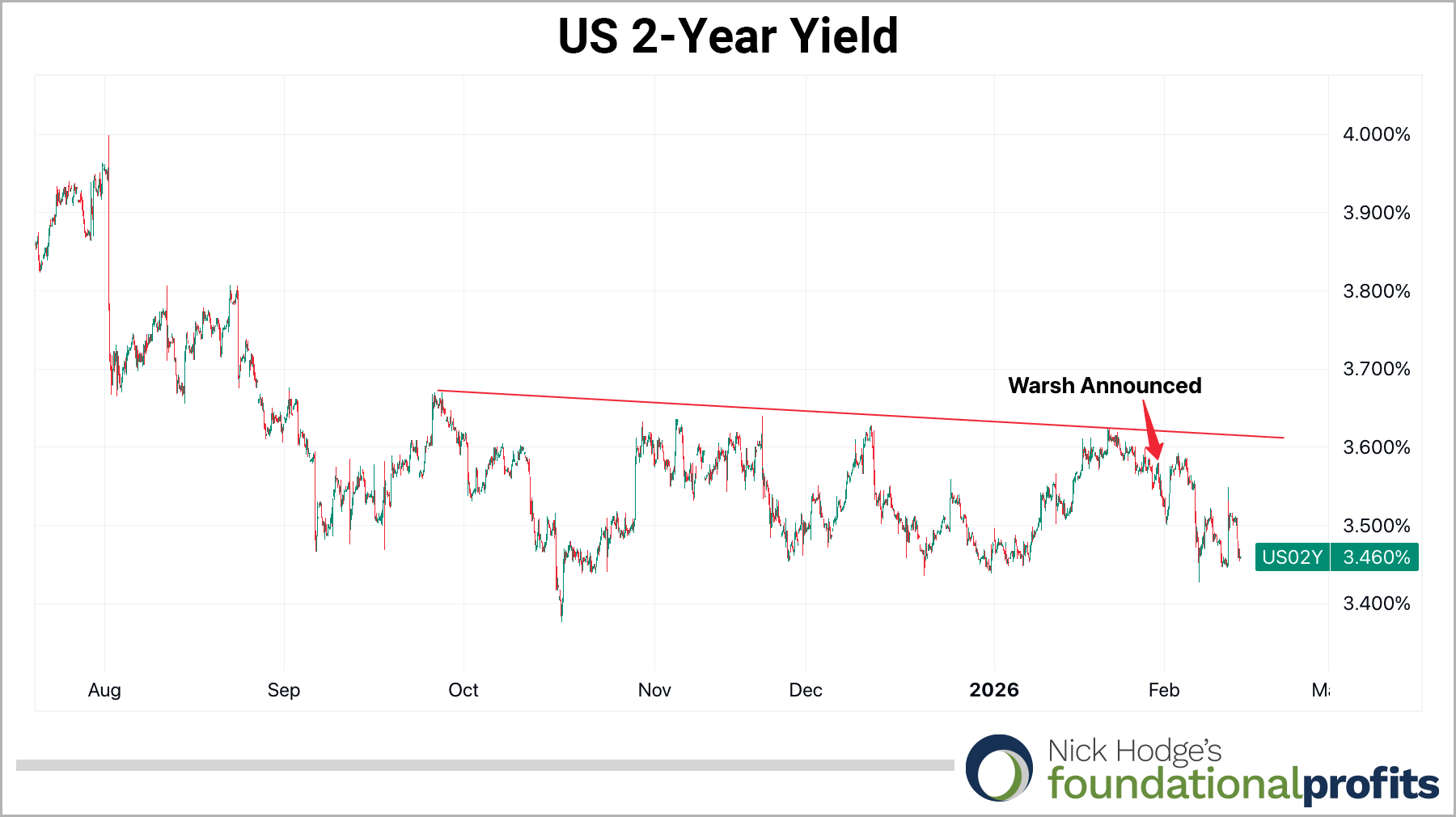

The US 2-Year yield is indicating rate cuts are likely on the way as well. It moved to three-month lows near 3.42% the week after Kevin Warsh was announced as the pick. It has moved slightly higher this week on a "stronger than expected” jobs report, which underscores that rate cuts aren’t imminent. But its refusal to make higher highs and break out of its downward trend tells me they are still on the way in the back half of this year, which will provide additional tailwinds for equities and metals even if we have to endure some chop before we get them.

We are long gold three ways.

We own gold via ETF. We own gold miners.

And we own gold this overlooked third way, by buying “Gold

Scripts,” which are a special type of contract that gives you massive leverage to rising gold prices...

Without any of the risks that crush most gold investors.

Click here to see how much better Gold Scripts outperform other gold investments.

Call it like you see it,

Nick Hodge

Publisher, Daily Profit Cycle