Nick Hodge,

Publisher

March 17, 2026

Editor’s Note: Please enjoy the macro update below, originally published as the intro to the March issue of Foundational Profits last Friday.

The data doesn’t say recession or bear market.

A new war may change that.

The news has been unfolding at a pace with which it’s hard to keep up. Let’s slow it down and check our reliable navigational beacons.

S&P is down ~2.7% year-to-date through March 12. Though it was down more than 1% in both January and February, this month’s selloff has been the most pronounced and feels different because it comes with war fog.

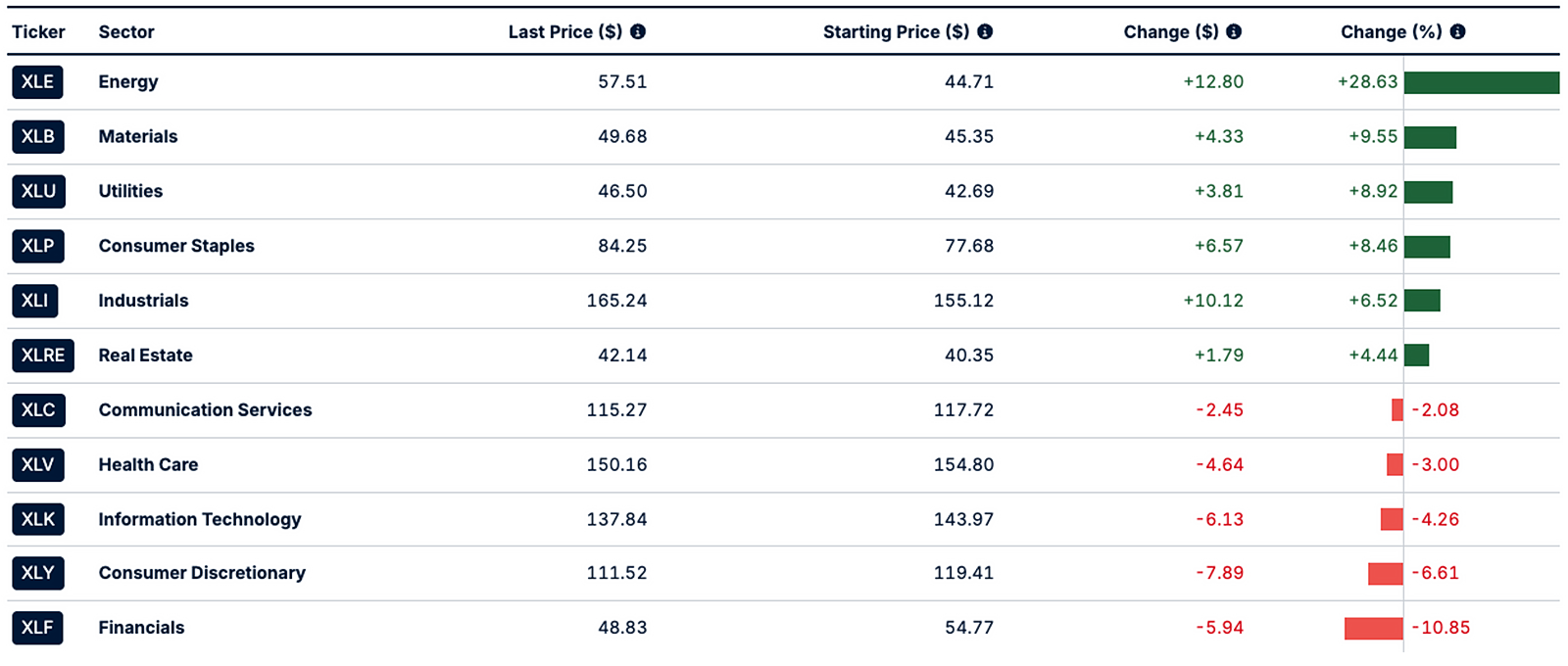

Sectors leading are: Energy (28.6%), Materials (9.6%), and Utilities (8.9%).

Sectors losing are: Financials (-10.9%), Consumer Discretionary (-6.6%), and Information Technology (-4.3%).

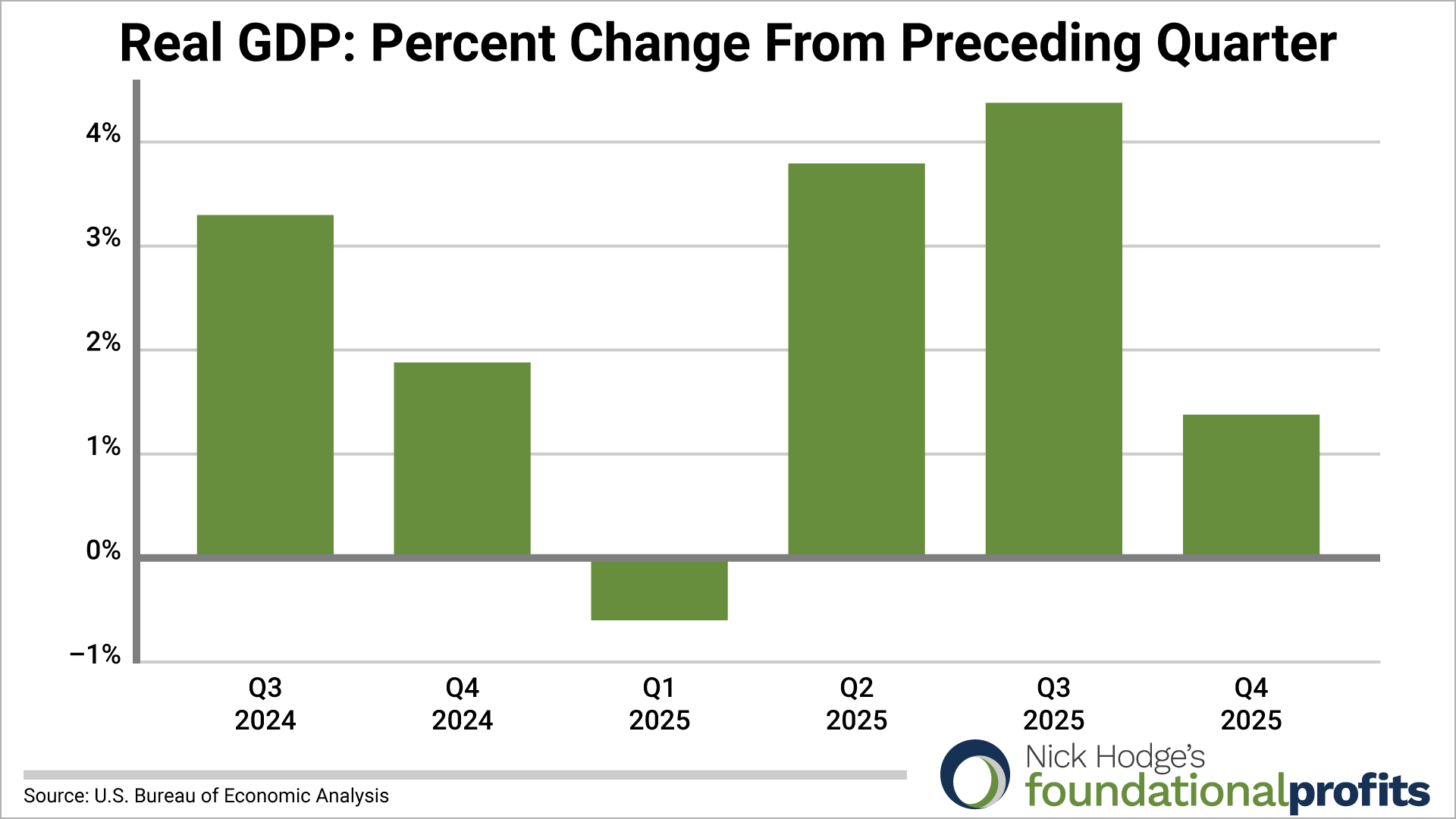

Slowing economic growth can be pointed to as the first non-war driver. I told you last month that “the economy is still expanding, but at a slower rate.” And that has turned out to be true. But it has slowed more than I and most others thought, with Q4 GDP coming out at 1.4%.

Changing inflation data is the more recent and war-driven culprit. Before bombs fell in Iran, expectations for inflation were largely flatlined at ~2.4%. With the spike in oil prices and some related commodities, many base case expectations for March monthly CPI have jumped near 2.8%, which would put us back to where we were last fall before inflation started falling.

The market does not like this stagflating scenario of middling economic growth and rising inflation. And with the added risk of wider war, capital has quickly turned defensive.

A strengthening dollar underscores the flight to relative safety, with the DXY up from ~96 in early February to over 99 this month on spikes.

Over the past couple weeks several major asset classes — oil, gold, bitcoin, and commodities — have correlated positively with this dollar strength. The S&P has correlated negatively.

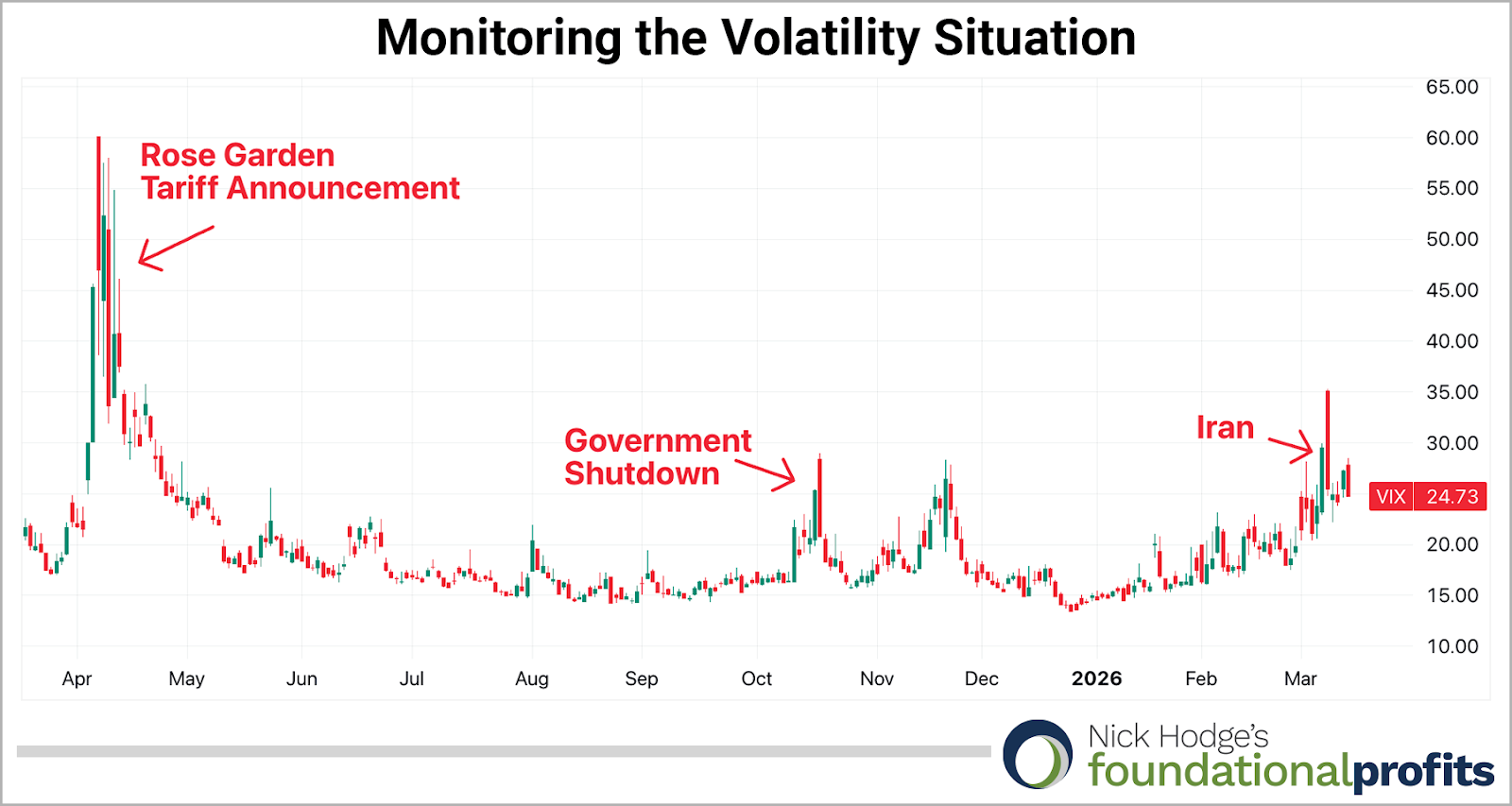

And the need to buy protection has led to a spike in the volatility index. It spiked briefly above 35 but is settling into levels comparable to that seen during the government shutdown of October 2025. It is still far from the Rose Garden tariff selloff of last spring, which saw spikes to 60, indicating this new war might not impact the markets for long.

The last big beacon is interest rates, which have been rising counter to their trend. The US10-Year yield has largely been trending lower since early 2025, putting in its lowest close of that period just a few weeks ago at the end of February at 3.95%. Since then, it has made a major upward move above the trendline. Rates are now flashing bullish. We’ll need to see if it holds.

Odds don’t favor a rate cut until the December meeting, now delayed several months after Jerome jumps ship and we get a new scallywag at the helm. Adding to the tardiness is a now-muddled broader economic picture with the aforementioned slowing growth and rising inflation.

As it is, until markets better understand the scope and duration of the new war, caution and defense are warranted.

And, in some cases, that stronger dollar and temporarily-rising yields have provided the need for some portfolio rotation and new entry.

Case in point: It’s another buy the dip moment for gold and select gold stocks.

Call it like you see it,

Nick Hodge

Publisher, Bizarro World