Gerardo Del Real,

Editor

Feb. 10, 2026

Markets have a way of telling you when leadership is changing.

You just have to be willing to listen.

Over the past year, the most crowded trade on the planet has been growth, technology, and anything remotely tied to artificial intelligence. Investors chased the obvious winners. Capital flooded into the same names. Valuations stretched. Expectations followed.

Now look at the scoreboard.

Information Technology and Communication Services are negative on the year, while Energy and Materials are leading the S&P. That’s not a coincidence. That’s rotation.

And at the center of that rotation sits one of the most misunderstood, under-owned, and structurally tight commodities in the market today: uranium.

Uranium Is Reasserting Itself as a Strategic Asset

According to Sprott’s latest outlook, uranium entered 2026 with renewed strength as spot prices pushed back into triple digits, climbing above $100 per pound in January. That move wasn’t speculative. It was a response to tightening fundamentals, delayed contracting, and policy-driven demand visibility that continues to extend further into the future.

More importantly, the move signaled a shift in investor focus.

For much of the last cycle, attention was concentrated downstream — reactor builders, nuclear utilities, and service providers. That narrative has matured. Capital is now moving upstream, toward the companies that actually produce the fuel required to keep reactors running.

That’s where uranium mining equities come in.

In January alone, uranium miners surged nearly 40%, and junior uranium stocks jumped more than 45%. On a one-year basis, miners are up roughly 95%, and juniors are up over 100%.

Those numbers dwarf broader equity and commodity benchmarks.

This is leadership.

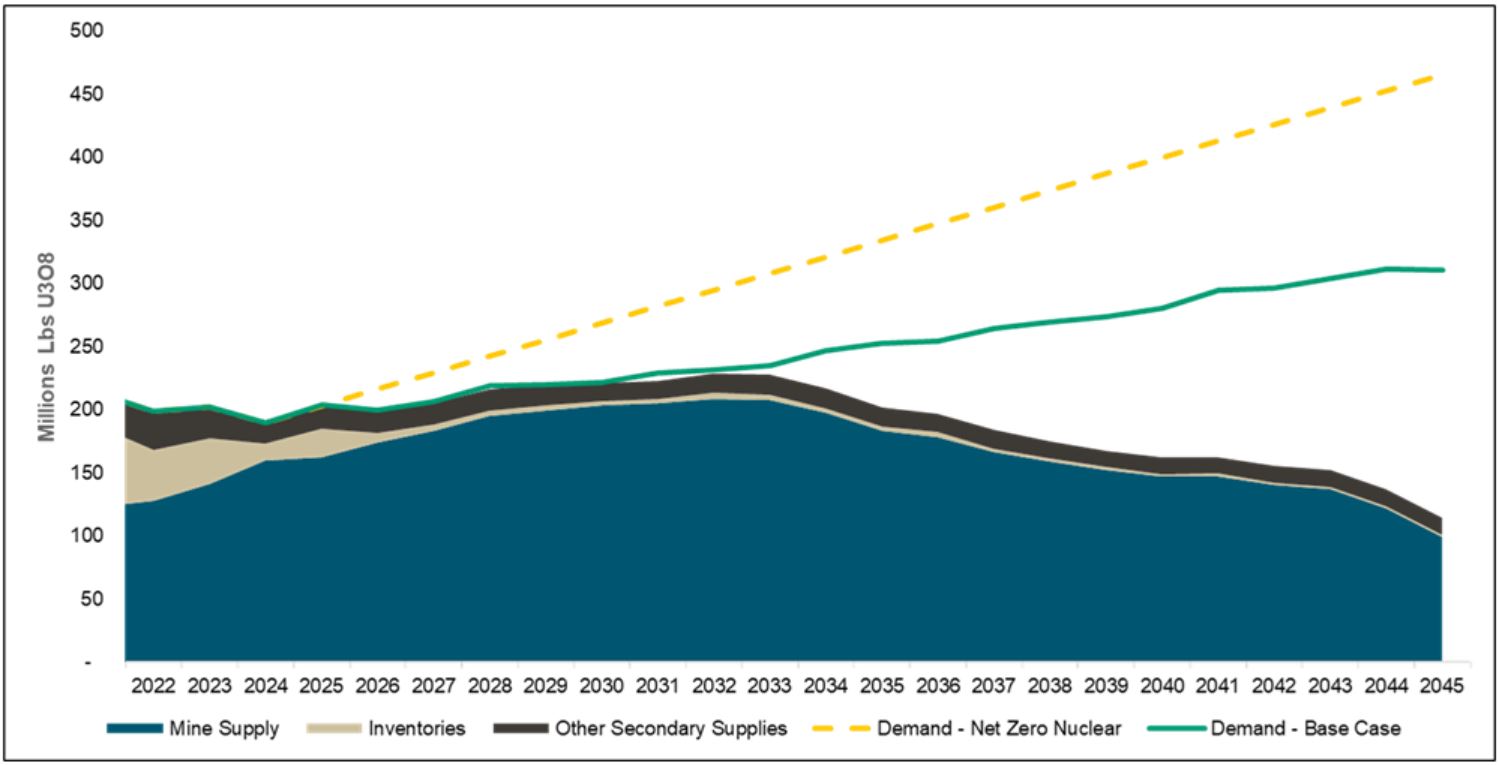

The Supply Side Remains the Real Story

The strongest bull markets are built on constraints. Uranium has them in abundance.

For more than a decade, utilities consistently under-contracted uranium. 2025 marked the 13th consecutive year in which long-term contracting fell short of replacement needs. That shortfall doesn’t disappear. It accumulates.

Even with a late-year pickup in contracting activity, total volumes remain below what’s required to cover future reactor demand. As Sprott notes, deferred procurement increases the likelihood that utilities will be forced back into the market later, with larger volumes to secure, fewer choices, and higher prices.

On the supply side, the picture is no better.

Kazakhstan — the world’s largest uranium producer — recently tightened control over exploration and development through Kazatomprom. The changes effectively raise the bar for new discoveries and reinforce state control over future production. That move alone sent a clear message to the market: cheap, unconstrained supply is not coming back anytime soon.

Globally, uranium production is concentrated in just a few jurisdictions. Kazakhstan, Canada, and Namibia account for nearly three-quarters of global mine output. New greenfield projects are scarce, underfunded, and slow to advance.

Higher prices are not optional. They are required.

Policy Has Entered the Equation in a Big Way

One of the most underappreciated catalysts for uranium in 2026 is policy.

In January, the U.S. issued a Section 232 proclamation identifying uranium as a critical mineral tied directly to national security. The implications are significant. The framework opens the door to trade adjustments, price-support mechanisms, and long-term incentive structures designed to secure domestic supply.

Layer on top of that the U.S. government’s stated goal to quadruple nuclear capacity by 2050, with 10 new large reactors targeted by 2030, and the demand picture becomes unmistakable.

Sprott estimates that achieving these goals would require an extraordinary amount of incremental uranium — potentially doubling today’s global production just to meet U.S. needs over time.

That kind of demand visibility changes everything.

AI and Data Centers Are the Optionality

Here’s where the narrative gets even more interesting.

Artificial intelligence, cloud computing, and data centers are rapidly increasing power demand. Reliability matters. Baseload matters. Nuclear fits.

But here’s the key point: the bull case for uranium does not depend on AI.

Even without factoring in incremental data-center demand, uranium faces a tightening supply-demand balance driven by electrification, energy security, and long-term reactor commitments already in place.

AI simply adds optionality.

It accelerates timelines. It sharpens urgency. It increases competition for fuel in a market that is already structurally short.

That’s exactly the kind of setup that produces sustained bull markets.

Why 2026 Matters

Uranium markets don’t move in straight lines. They move in phases.

Sprott describes uranium’s history as a series of consolidations followed by sharp repricing once participation returns. January’s move back above $100 per pound looks like the start of another such phase.

Term prices are rising. Contracting is re-engaging. Policy support is aligning. Supply discipline remains intact.

Meanwhile, capital is rotating out of last cycle’s winners and into real assets with leverage to scarcity.

That’s why I believe 2026 could be a defining year for uranium investors.

Not because the story is new — but because the market is finally starting to price it correctly.

Where the Opportunity Is Now

Owning uranium is one thing.

Owning the right uranium companies is another.

The next phase of this bull market won’t reward everything equally. Quality projects, credible management teams, and jurisdictions that can actually deliver pounds into a tightening market will matter more than ever.

That’s where my focus is.

I’ve been positioning for this setup for some time, and I’m actively recommending specific uranium stocks that I believe are best positioned for the next leg higher.

If you want to see exactly which names I’m buying now — and why — you can find that information right here.

Let's get it,

Gerardo Del Real

Editor, Daily Profit Cycle